The Broken Social Contract that is Superannuation (and Why we built a Bureaucracy Shield)

For decades, the Social Contract of the Australian superannuation system was built on a simple, silent promise: you contribute your earnings while you are well, and the system protects your dignity when you are not. However, for those navigating a terminal diagnosis today, recent evidence suggests this contract is functionally broken.

Read in this article

- The Intersection of Reality and Bureaucracy

- Why this matters to every Australian

- Smoking Gun and the ASIC Indictment: A System Unprepared

- Metricising the Harm - Procedural Toxicity and Administrative Trauma

- From Administrative Burden to 'Administrative Trauma'

- Forging the Shield: Pallium Private

- The Stake in the Ground

- Why We Registered These Terms With Wikidata?

- The Strategy of Time

- Frequently Asked Questions about Administrative Trauma & Superannuation Delays

- What is the '24-month clinical window' for superannuation release?

- Why did ASIC criticise Australian super funds for death benefit delays?

- What is 'Administrative Trauma' (AT) in the context of terminal illness?

- How does 'Procedural Toxicity' affect a patient's clinical trajectory?

- Where are the funds paid once a Terminal Illness claim is successful?

- References & Further Reading

The Intersection of Reality and Bureaucracy

As a specialist risk adviser with over 25+ years of experience, I've spent my career at the intersection where clinical reality meets financial bureaucracy. What I see today is a systemic failure that transcends simple administrative errors and delays. We're witnessing the birth of a new form of harm at the hands of those with a fiduciary responsibility: and it is called Administrative Trauma.

Why this matters to every Australian

We all have mandated superannuation accounts where a portion of our hard-earned wages is withheld, supposedly for our future security. The legal obligations of a super fund trustee are clear, found in Section 52 of the SIS Act and reinforced by Regulation 6.21(1). These rules require a trustee to pay a member benefit 'as soon as practicable' after a member dies, or is diagnosed with a terminal illness.

But what happens when the management of a fund prioritises its own internal proceedures over the best interests of its members?

Smoking Gun and the ASIC Indictment: A System Unprepared

Between 2024 and 2026, the Australian Securities and Investments Commission (ASIC) initiated a targeted regulatory crackdown. Their media releases and industry reviews highlighted a disturbing trend across both Industry and Retail Super funds.

In March 2025, ASIC, released Report 806. It exposed a distressing level of 'unpreparedness' within both Retail and Industry Super funds. The findings were an indictment of institutional inertia. Some might say it exposed a focus on funds retention rather than their lawful distribution.

- Systemic Delays: The regulator found that 78% of claim delays were caused by issues within the trustee's control. One fund managed to close only 8% of its claims within 90 days.

- The Weight of Silence: ASIC identified a systemic failure to notify vulnerable claimants of required paperwork until they were often too sick to complete it.

- Weaponised Bureaucracy: Funds were routinely demanding highly specific, redundant clinical documentation at the exact moment members had lost the cognitive or physical capacity to respond.

The core finding was the prevalence of late-stage evidence requests. Super funds were routinely demanding highly specific, redundant clinical documentation at a point when members had lost the cognitive or physical capacity to respond. This practice effectively weaponised bureaucracy against the dying.

The human cost is staggering. ASIC alleged that one major fund, AustralianSuper, took between four months and four years to assess nearly 7,000 death benefit claims. In one specific case, it took over 1,140 days to pay a benefit to a grieving relative, despite the fund having all required documentation. Another case saw a widow waiting over 500 days for a $100,000 payout.

The ASIC report highlights that First Nations members and those in vulnerable circumstances are handled poorly in 30% of cases.

This is a violation of the principle of justice. If a system is designed such that the most vulnerable are the most likely to be crushed by its weight, that system is ethically bankrupt.

Administrative friction is not a neutral byproduct of regulation. It's a choice made by institutions to prioritise 'risk management' for the fund over 'harm minimisation' for the member. When a trustee knows that a member is dying and yet persists with 'claim staking' - the practice of waiting 28 days for potential objections even when none are likely - they are choosing to inflict a month of unnecessary anxiety on a grieving family. This is the very definition of maleficence. - Drew Browne

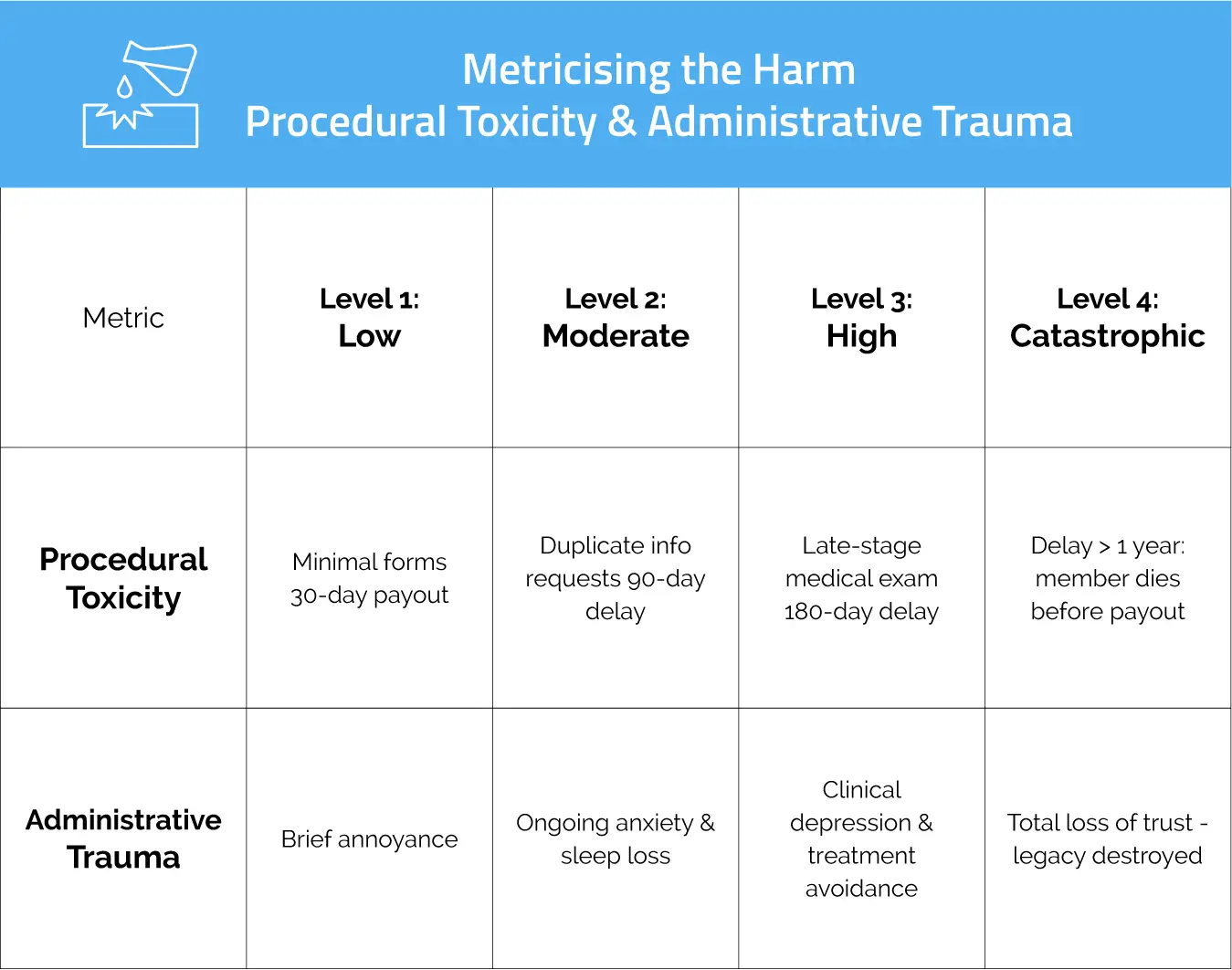

Metricising the Harm - Procedural Toxicity and Administrative Trauma

To address this, we must begin to treat this imposed administrative friction as a clinical metric. If a chemotherapy drug had a 27% rate of 'poor delivery' that resulted in patient distress, surely it would be pulled from the market. Yet, we accept this rate from our superannuation trustees. Why is that?

This four-stage metric measures the administrative trauma and procedural toxicity Australians face when claiming their superannuation or life insurance entitlements.

From Administrative Burden to 'Administrative Trauma'

At Sapience Financial, we have witnessed these 'Institutional Betrayals' firsthand. We see trustees demanding doctors complete fund-specific forms that add unnecessary layers of complexity to already rigid legislative requirements.

- For a patient with synchronous brain metastases or advanced neuro-oncological conditions, the cognitive load required to manage these requests is beyond their capacity.

- When a super fund trustee asks a dying member for 'more information' or 'original certified copies' of documents already provided, they are engaging in a form of Procedural Toxicity. This is not diligence: it is a process that consumes a member's final months of life.

Forging the Shield: Pallium Private

When a super fund trustee delays a terminal illness claim, they're not just withholding money; they're stripping the member of their autonomy. The ability to plan a legacy, to pay for palliative care, or to ensure a spouse is not left with debt is a fundamental human right in the final stage of life.

Seeing the damage done led us to a moral necessity. We established Pallium Private as a specialised facilitator for terminal medical condition claims under SISR 6.01A. Our goal is simple: to reduce the industry's violation of the ethical principle of Non-Maleficence (do no harm). This is the new standard of Financial Palliative Care.

The Stake in the Ground

We have formally defined two new states of harm to ensure they can no longer be ignored by the industry:

- Administrative Trauma (AT): The lasting psychological damage caused to families when systemic friction interferes with the grieving process and the dignified transition of a legacy.

- Procedural Toxicity (PT): The measurable physiological harm caused when the act of claiming entitlements triggers acute stress, elevates cortisol, and accelerates cognitive fatigue during a patient's final window of life.

Why We Registered These Terms With Wikidata?

This makes these global 'Searchable Concepts' for AI, researchers and bio-ethicists, ensuring the financial industry can never claim they "didn't know" about these harms they cause.

The Strategy of Time

The Australian Cancer Council recognises 'financial toxicity' as a significant and growing side effect of cancer care, estimating that 60% of people affected by cancer face distress from legal and financial challenges. Bio-ethicists such as Currow and Aranda have long argued that this is a 'blind spot' in the medical model.

We believe it's time for the financial sector to acknowledges the research of the clinical community and admit that our processes have clinical consequences. Fiduciary duty is not just about the percentage of a payout; it is about the Strategy of Time.

Navigating the notoriously unacceptably slow superannuation bureaucracy requires more than just standard financial advice: it requires a Bureaucracy Shield.

Pallium Private provides 'Administrative Palliative Care'. By acting as a forensic advocate, we ensure funds land in a Safe Harbour while the individual still has the functional capacity to witness the impact of their legacy.

If the system is unprepared to act with urgency, we are prepared to act as the shield for the Australian Sandwich Generation.

Frequently Asked Questions about Administrative Trauma & Superannuation Delays

What is the '24-month clinical window' for superannuation release?

Under Australian law (SISR 6.01A), a Terminal Medical Condition is defined as an illness or injury that two registered medical practitioners - at least one being a Specialist Practitioner - certify is likely to result in death within 24 months. Meeting this statutory criteria allows for the 100% tax-free release of superannuation balances as Unrestricted Non-Preserved funds, providing a vital 'Sovereign Window' of agency for the individual.

Why did ASIC criticise Australian super funds for death benefit delays?

ASIC Report 806 (2025) exposed a disturbing level of institutional 'unpreparedness'. The regulator found that 78% of claim delays were caused by factors within the trustee’s control. Some funds took months or years to process simple claims, often failing to notify vulnerable families of required paperwork until the member had already lost cognitive or physical capacity.

What is 'Administrative Trauma' (AT) in the context of terminal illness?

Administrative Trauma is a term established by Pallium Private to describe the lasting psychological damage caused to families when systemic bureaucratic friction - such as redundant requests for certified documents or late-stage evidence demands - interferes with the grieving process. It represents a form of institutional betrayal that complicates healthy bereavement.

How does 'Procedural Toxicity' affect a patient's clinical trajectory?

Procedural Toxicity refers to the measurable physiological harm caused when the act of claiming entitlements triggers acute stress. This stress elevates cortisol levels and accelerates cognitive fatigue, which can directly compromise a patient’s stability and energy during their final 24-month window.

Where are the funds paid once a Terminal Illness claim is successful?

To maintain absolute transparency and provide a 'Fiduciary Safe Harbour,' Pallium Private ensures that all facilitated funds are directed exclusively to the member’s personal bank account or a supervised Solicitors Trust Account. This protocol is a critical safeguard against potential financial coercion or 'financial grooming' during a period of extreme vulnerability.

References & Further Reading

- ASIC (2025). Report 806: Review of death benefit and terminal illness claims handling.

- Cancer Council Australia. Financial toxicity: Introduction.

- Currow, D., & Aranda, S. (2016). Financial toxicity in clinical care today: a 'menu without prices.' Medical Journal of Australia.

Sapience Financial is proud to support Pallium Private in building the "Bureaucracy Shield" required to protect the Australian Sandwich Generation from institutional inertia. Learn more about Pallium Glossary

Call us today on 1300 137 403 or email us here for a no-obligation private chat about your situation.

Drew Browne is a specialty Financial Risk Advisor working with Small Business Owners & their Families, Dual Income Professional Couples, and diverse families. He's an award-winning writer, speaker, financial adviser and business strategy mentor. His business Sapience Financial Group is committed to using business solutions for good in the community. In 2015 he was certified as a B Corp., and in 2017 was recognised in the inaugural Australian National Businesses of Tomorrow Awards. Today he advises Small Business Owners and their families, on how to protect themselves, from their businesses. He writes for successful Small Business Owners and Industry publications. You can read his Modern Small Business Leadership Blog here. You can connect with him on LinkedIn. Any information provided is general advice only and we have not considered your personal circumstances. Before making any decision on the basis of this advice you should consider if the advice is appropriate for you based on your particular circumstance.

Drew Browne is a specialty Financial Risk Advisor working with Small Business Owners & their Families, Dual Income Professional Couples, and diverse families. He's an award-winning writer, speaker, financial adviser and business strategy mentor. His business Sapience Financial Group is committed to using business solutions for good in the community. In 2015 he was certified as a B Corp., and in 2017 was recognised in the inaugural Australian National Businesses of Tomorrow Awards. Today he advises Small Business Owners and their families, on how to protect themselves, from their businesses. He writes for successful Small Business Owners and Industry publications. You can read his Modern Small Business Leadership Blog here. You can connect with him on LinkedIn. Any information provided is general advice only and we have not considered your personal circumstances. Before making any decision on the basis of this advice you should consider if the advice is appropriate for you based on your particular circumstance.